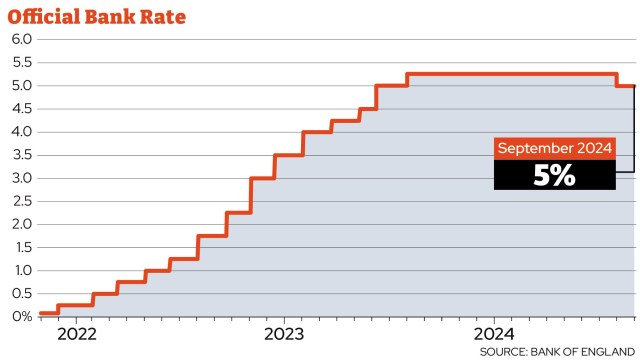

The Bank of England has held interest rates at 5 per cent.

The Bank’s Monetary Policy Committee (MPC) made the first reduction since March 2020 last month, reducing the rate by 0.25 percentage points.

However, it voted by a majority of 8–1 to maintain the base rate at 5 per cent today, as inflation remains sticky. One member of the MPC preferred to reduce Bank Rate by 0.25 percentage points, to 4.75 per cent.

Yesterday, figures released by the Office for National Statistics (ONS) showed inflation stayed at 2.2 per cent.

While near the Bank’s 2 per cent target, the Bank remains cautious about cutting interest rates too quickly.

Andrew Bailey, the Bank of England’s governor, said: “It’s vital that inflation stays low, so we need to be careful not to cut too fast or by too much.”

When will the base rate fall again?

Economists generally expect the base rate to fall again at the next meeting in November with some also expecting another drop in December.

It would likely be another 0.25 percentage point drop, taking the rate to 4.75 per cent.

Rob Wood, chief UK economist at Pantheon Macroeconomics, said: “The MPC remains on track to cut rates again later this year – we think in November – as underlying services inflation continues to trend down.”

This was also alluded to in the Bank’s minutes. It said: “In the absence of material developments, a gradual approach to removing policy restraint remains appropriate.”

However, the change will be dependent on what happens to inflation rates.

What will happen to inflation?

While it was revealed that inflation stayed the same as last month’s figure of 2.2 per cent, and is near the Bank’s 2 per cent target, services inflation – which includes hospitality costs and air fares – rose from 5.2 per cent to 5.6 per cent.

Core inflation, which excludes volatile measures such as energy, food, alcohol and tobacco, also rose by 3.6 per cent in the 12 months to August 2024, up from 3.3 per cent in July.

Many economists expect inflation to rise higher, with a Bank forecast suggesting it will reach 2.5 per cent by the end of this year.

With inflation higher, it may be more difficult for the Bank to bring down interest rates quickly.

What does a rate hold mean for mortgage holders and renters?

Those on tracker or standard variable rate mortgages, which tend to follow the base rate, will see no change after today’s announcement.

However, they are coming down, on average. A typical standard variable rate (SVR) has fallen below 8 per cent for the first time since August 2023 when it was 7.85 per cent. It now stands at 7.99 per cent, down from 8.18 per cent in March 2024.

Some 81 per cent of people are on fixed-rate mortgages, where the interest rate is locked in for a set period of time, so if you are on this type of loan, your repayments will not change based on the decision.

These rates have come down in recent months since a peak last summer, but depending on when you locked into a fix rate, you are likely to be paying a higher rate when you come to renew than you were before.

Both two- and five-year fixed deals now available for below 4 per cent but many will be moving off rates that were as low as one per cent.

However, experts expect rates to continue to come down.

Nick Mendes of brokers John Charcol said: “The gap between two and five year fixed mortgage rates is expected to narrow.

“By the end of 2024, five year rates could drop to around 3.5 per cent while two year rates are expected to be around 3.8 per cent. As lenders respond to lower funding costs and increased competition, we could see even more attractive mortgage deals. “

The best deals currently available are for those with high equity or deposits but this could also change.

Mendes added: “Mortgage rates for higher loan to values (LTV) of 90 to 95 per cent could potentially reach around 4.5 per cent by the end of the year. This would provide financial relief to homeowners, encourage first-time buyers, and motivate home movers, boosting both the housing market and the wider economy.”

If you’re approaching the last six months of your fixed-rate mortgage, experts recommend that now is the time to start exploring new deals.

However, some lenders have reduced how far ahead you can lock in a deal. For instance, Nationwide still offers 180 days, but others like Santander and Halifax have shortened theirs to 120 days.

Renters, meanwhile, are indirectly affected by landlords’ mortgage costs. It remains to be seen whether these costs decrease, but if they do, it is unlikely to be immediate, as plenty of landlords will still be remortgaging this year and next, seeing steep increases that they may pass on.

Research this week showed that the increase in private rents is almost four times that of inflation, according to the Office for National Statistics (ONS), climbing to a near-record rate to 8.4 per cent in the year to August.

What does it mean for savers?

Higher interest rates overall mean higher returns for savers.

One of the best easy access deals currently on the market is with Ulster Bank at 5.2 per cent followed by Oxbury Bank at 4.87 per cent. The best one year fixed rate account is with Gatehouse Bank at 4.85 per cent.

Although the rates are higher than inflation, they have come down from their peak when savings rates were well above 5 per cent.

The average easy access rate has fallen from 3.15 per cent since August 2024 to 3.08 per cent in September.

Experts suggest those looking to get the best returns on their savings lock in a rate now to ensure they get the best possible deal.

If you opt for a fixed rate rather than an easy-access rate, the interest will be guaranteed for the term of the deal, meaning you can be certain your returns will beat inflation.

Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, said: “There is an expectation that base rate will be cut twice more before the year is over, so savers need to prepare themselves for more interest rate cuts. Those who are happy to lock their cash away for a guaranteed return could look towards a fixed rate bond or fixed Cash ISA, and with rates expected to decrease further, savers may wish to choose a longer-term deal.”