Bid–ask spread

The bid–offer spread (also known as bid–ask or buy–sell spread (in the case of a market maker), and their equivalents using slashes in place of the dashes) for securities (such as stocks, futures contracts, options, or currency pairs) is the difference between the prices quoted (either by a single market maker or in a limit order book) for an immediate sale (bid) and an immediate purchase (offer). The size of the bid-offer spread in a security is one measure of the liquidity of the market and of the size of the transaction cost.[1] If the spread is 0 then it is a frictionless asset.

Contents

Liquidity

The trader initiating the transaction is said to demand liquidity, and the other party (counterparty) to the transaction supplies liquidity. Liquidity demanders place market orders and liquidity suppliers place limit orders. For a round trip (a purchase and sale together) the liquidity demander pays the spread and the liquidity supplier earns the spread. All limit orders outstanding at a given time (i.e., limit orders that have not been executed) are together called the Limit Order Book. In some markets such as NASDAQ, dealers supply liquidity. However, on most exchanges, such as the Australian Securities Exchange, there are no designated liquidity suppliers, and liquidity is supplied by other traders. On these exchanges, and even on NASDAQ, institutions and individuals can supply liquidity by placing limit orders.

The bid–offer spread is an accepted measure of liquidity costs in exchange traded securities and commodities. On any standardized exchange, two elements comprise almost all of the transaction cost—brokerage fees and bid-offer spreads. Under competitive conditions, the bid-offer spread measures the cost of making transactions without delay. The difference in price paid by an urgent buyer and received by an urgent seller is the liquidity cost. Since brokerage commissions do not vary with the time taken to complete a transaction, differences in bid-offer spread indicate differences in the liquidity cost.[2]

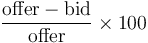

Percent spread

Percent spread is  .

.

Example: Currency spread

If the current bid price for the EUR/USD currency pair is 1.5760 and the current offer price is 1.5763, this means that currently you can sell the EUR/USD at 1.5760 and buy at 1.5763. The difference between those prices (3 pips) is the spread.

If the USD/JPY currency pair is currently trading at 101.89/101.92, that is another way of saying that the bid for the USD/JPY is 101.89 and the offer is 101.92. This means that currently, holders of USD can sell 1 USD for 101.89 JPY and investors who wish to buy dollars can do so at a cost of 101.92 JPY per 1 USD.

See also

References

- ↑ Spreads – definition

- ↑ Demsetz, H. 1968. "The Cost of Transacting." Quarterly Journal of Economics 82: 33–53 http://web.cenet.org.cn/upfile/100078.pdf doi:10.2307/1882244 JSTOR 1882244

Further reading

- Lua error in package.lua at line 80: module 'strict' not found.