Weighted average cost of capital

Lua error in package.lua at line 80: module 'strict' not found. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. The WACC is commonly referred to as the firm’s cost of capital. Importantly, it is dictated by the external market and not by management. The WACC represents the minimum return that a company must earn on an existing asset base to satisfy its creditors, owners, and other providers of capital, or they will invest elsewhere.[1]

Companies raise money from a number of sources: common stock, preferred stock, straight debt, convertible debt, exchangeable debt, warrants, options, pension liabilities, executive stock options, governmental subsidies, and so on. Different securities, which represent different sources of finance, are expected to generate different returns. The WACC is calculated taking into account the relative weights of each component of the capital structure. The more complex the company's capital structure, the more laborious it is to calculate the WACC.

Companies can use WACC to see if the investment projects available to them are worthwhile to undertake.[2]

Calculation

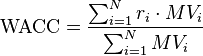

In general, the WACC can be calculated with the following formula:[3]

where  is the number of sources of capital (securities, types of liabilities);

is the number of sources of capital (securities, types of liabilities);  is the required rate of return for security

is the required rate of return for security  ; and

; and  is the market value of all outstanding securities .

is the market value of all outstanding securities .

In the case where the company is financed with only equity and debt, the average cost of capital is computed as follows:

where D is the total debt, E is the total shareholder’s equity, Ke is the cost of equity, and Kd is the cost of debt. The market values of debt and equity should be used when computing the weights in the WACC formula.[1]

Tax effects

Tax effects can be incorporated into this formula. For example, the WACC for a company financed by one type of shares with the total market value of  and cost of equity

and cost of equity  and one type of bonds with the total market value of

and one type of bonds with the total market value of  and cost of debt

and cost of debt  , in a country with corporate tax rate

, in a country with corporate tax rate  , is calculated as:

, is calculated as:

Actually carrying out this calculation has a problem. There are many plausible proxies for each element. As a result, a fairly wide range of values for the WACC for a given firm in a given year, may appear defensible.[4]

See also

- Beta coefficient

- Cost of capital

- Discounted cash flow

- Economic Value Added

- Internal rate of return

- Minimum acceptable rate of return

- Modigliani-Miller theorem

- Net present value

- Opportunity cost

References

- ↑ 1.0 1.1 Fernandes, Nuno. 2014, Finance for Executives: A Practical Guide for Managers, p. 32. Cite error: Invalid

<ref>tag; name "Nuno_Fernandes" defined multiple times with different content - ↑ Lua error in package.lua at line 80: module 'strict' not found.

- ↑ Lua error in package.lua at line 80: module 'strict' not found.

- ↑ Lua error in package.lua at line 80: module 'strict' not found.

External links

- Video about practical application of the WACC approach

- Lua error in package.lua at line 80: module 'strict' not found.

- Lua error in package.lua at line 80: module 'strict' not found.

- Lua error in package.lua at line 80: module 'strict' not found.

- A rather complete WACC calculator

- Another very basic WACC calculator

- A more realistic valuation: APV and WACC with constant book leverage ratio

- Calculate the WACC with your own values to understand the equation

- Find the WACC of any publicly traded company by entering the firm's stock ticker symbol

- Paper describing a method for generating the WACC curve when there is default risk – spreadsheet available

- Tutorial how to calculate WACC in Excel.